|

Health is Wealth. Everyone has heard this adage. In today’s world with the rising costs of health care and medical facilities, this saying is doubly true. In the modern age we are at risk for increased health problems to the increasing pollution and hazards of modern living.

Therefore, it is crucial for us to have a good health insurance plan that provides Family Health Insurance Plans and also covers all our health care expenses. We are constantly worried about the well-being and health of our family. Getting good Family Health Insurance Plans can go a long way in alleviating such concerns. More and more people today are opting for family floater health insurance plans rather than individual covers. Best Family Health Insurance Plans Available Online ICICI Lombard Complete Family Health Insurance Plans - provides comprehensive coverage for you and your family. The policy also offers customization as per the insurer’s needs taking factors like hospitalization and maternity cover into play. Policy Coverage

Merits of Family Health Insurance Plans

Demerits of Family Health Insurance Plans

Max Bupa Heartbeat – is a family floater plan that provides complete blanket coverage for the health care of your family. Policy Coverage

Policy Coverage

Policy Coverage

Tata AIG- has Family Health Insurance Plans that provide each family member with independent coverage. There are three main plans-Classic, Supreme and Elite. Policy Coverage

Policy Name Entry-Exit Age Cap Sum Assured Limit ICICI Lombard Complete Health Insurance – iHealth Plan 3 months- No limit 3,00,000- 10,00,000 Max Bupa Heartbeat No lower or upper limit 2,00,000- 50,00,000 Star Health Family Health Optima 5 months- 65 years 1,00,000- 15,00,000 The Oriental Insurance Happy Family Floater 3 months- No limit 1,00,000- 5,00,000 (Silver) 6,00,000- 10,00,000 (Gold) Tata AIG Wellsurance Family 6 months- 65 years 2,00,000- 4,00,000

2 Comments

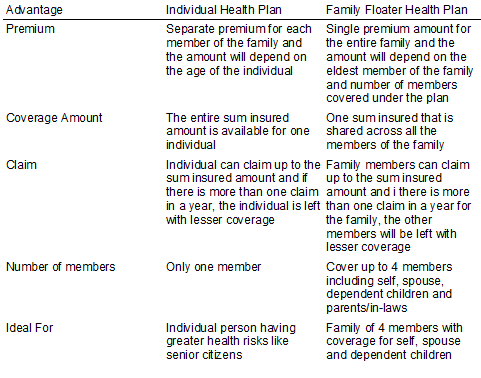

Health insurance plans act as a great saviour to protect an individual from any financial burden arising out of hospitalization and illnesses. The best way to protect your entire family under a single health plan is by opting for family floater plans.

Family floater plans help safeguards all the members of your family on a shared basis and with no individual limit for each member. The points mentioned below will assist you to understand in detail about family health plans, its key features and benefits. What is Family Health Plan? As opposed to individual health plans, family health plans covers the entire family under a single plan. It works with the prime assumption that all the members of the family will not fall ill at the same time or will have hospitalization expenses. If any member gets hospitalized, they can claim coverage up to the entire sum insured amount and thereby gain from a wider coverage. Differences between Individual and Family Health Plans How to Select the Best Family Health Plans? Choosing the right family health plan for your family depends on your family and their individual health requirements, dependencies and financial needs. Here are some points that will help you choose the right family health plan: 1. Sum Insured Selecting the right sum insured or coverage amount for the entire family is very important. Consider the number of members and their age, and choose the right sum insured amount for the family health plan. Even if one member gets hospitalized, there should be enough amount left for other members who might be at risk. 2. Age Older individual carry a higher health risk since they are more prone to diseases when compared to younger individuals. When you plan to cover your elderly parent or in-law under your family health plan, their age will determine the amount of premium you would pay. The higher the age of that member, the higher the premium will be. Also, there are possibilities that the elder member might use up a large part of the shared sum insured amount of the family health plan. Hence it is always recommended to buy a separate health plan for senior citizens, parents/in-laws. 3. Sub Limits Ensure that the family health plan does not have any sub-limits or specific limits for certain illnesses or treatments. Also check if there any room expense limit and reduce your out of pocket burden. Do, check out the exclusions, pre-existing diseases coverage and other clauses of the family health plan, before you make your purchase. 4. Premium A premium for a family health plan would definitely cost you lesser than separate individual healths for each member. Compare and select the best family health plan with a competitive premium rate and wider coverage. All in all, health insurance should not be considered as an unwanted expenditure. Having adequate health coverage is a must to protect you and your family. The best family health plans will reduce your burden and save your expenses by sharing cost across all the members of your family. Consider the above factors when selecting the best family health plan that is suitable for your family needs and requirements.  Royal Sundaram offers unparalleled health insurance plans that have a wide health coverage at affordable prices. Royal Sundaram Health Insurance called Lifeline is an individual and family covering insurance policy that is easy to comprehend and buy.

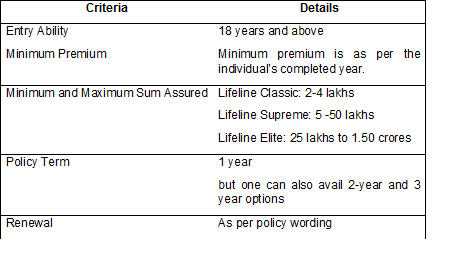

It covers you and your family for most of the medical calamities that might one might incur. An Overview of Royal Sundaram Health Insurance or Lifeline With access to the Royal Sundaram Health Insurance Login one can easily check out the options they offer to their clients. When one wants to insure their family, all one has to do is match the Royal Sundaram health insurance premium chart to the eldest person in the family and decide on the best suited plan. Before opting for this insurance policy let us look at some of the basic criteria that it covers. Why should you buy Royal Sundaram Health Insurance Lifeline? It offers benefits such as:

Features & Benefits of Royal Sundaram Health Insurance Lifeline Plan Apart from the regular covers like inpatient care, pre-and-post hospitalization expenses, it also covers vaccination expenses from animal bite, global emergency hospitalization and treatment of 11 critical illnesses excluding Canada and US. There is also a 7.5 percent discount on two year policy and 12 percent discount on a 3 year policy. For further details, contact the company’s customer care. What is the eligibility criteria to avail the insurance?

What are the inclusions or fine print in the insurance?

What are the exclusions or fine print in the insurance?

For more information, check the prospectus. Documents Required for Medical Reimbursement

How to make a claim?

For cashless facility

For reimbursement facility

For international treatment claims, refer to the company’s website for more information and clarification.  Accidents occur out of nowhere, a serious injurious or in worse cases, death could have serious financial consequences for one’s family. Financial security to your family in these situations is what accidental insurance plans provide.

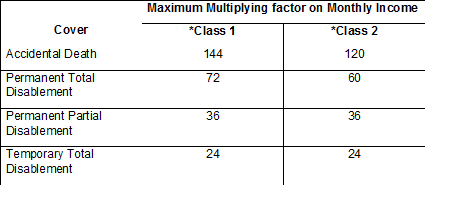

Overview of the Accidental Insurance Plan Many people generally opt for a lifetime Insurance Plan by Future Generali but a personal accidental insurance plan is more recommended as the person insured will be covered at a nominal premium rate. Covering the person in case of small injuries and loss of income as well. Normal life insurance plans do not cover these factors.. The entry age for the Insurance plan is 18 years to 70 years with a lifetime renewal option. For children 5 years to 25 years can be covered as dependents. The returned sum from the accidental insurance plan can be 100% to 1% depending on the type of injury that the policyholder or the members of the policy have sustained. 100% sum assured being for serious injuries like death while 1% per week for temporary total disablement. Why to buy Personal Accident Insurance Plan by Future Generali?

Key benefits and features of accidental insurance plan include a cashless claim network where there is a cashless claim service over 1000+ authorized network across India. There is a discount available for policyholders who are buying large sum policies there is a discount available up to 40 lakhs. A personal discount of Rs. 50 lakhs only for registered owner is also included in the benefits of buying Accidental Insurance Plans. Inclusions of Accidental Insurance Plan

There are many ways in which an Individual can apply for Accidental Insurance Plan from future Generali. They can log onto the company website and opt for the health Insurance plans that suits them the best. Individuals that are interested in the accidental insurance plans can call the Sales helping of the company and ask customer care how to go over the process of getting a policy. Claims Process for Accidental Insurance Plan At Future Generali, there is an in-house claim settlement team that processes claims within 14 working days from the time of receiving the completed claim documents. This team can also give specialized advice on how to go about the claiming process. For periodic updates one needs to mention their mobile and email-id so that they can follow their claims process. For getting claims for this Accidental Insurance Plan there are certain documents that are required to be submitted. These documents include the filled-up claims form that must be signed by the policyholder, a medical certificate from the medical center/doctor, a summary from the nursing hospital and also the original discharge card. Consultation of the Doctors history along with all ordinal reports, cash memos from the pharmacies/hospital along with proper prescriptions. The Medico Legal Certificate given for accidents. Rising medical care costs are the major reason why you need to buy Mediclaim policy for your family in the year 2017. Medical care costs are continuously rising every day, which becomes unbearable for middle class people in our country. A Mediclaim plans help you to manage your financial requirements at the time of medical emergency.

It is true that no one can predict about such uncertainties of life, but all you can do is that be prepared for any such unfortunate events that needs huge sum of money. As you are already stepped in to the year 2017 with lots of new resolutions, it is advised to add one more resolution to your list, which is buying a Medicalim policy for your family. It is very mandatory to protect yourself from the financial loss in case you or your family member meets any medical emergency. The best Mediclaim plan is one which offers right type of insurance coverage and benefits at nominal premium value according to the need of the individual. While selecting a family floater plan for your family amongst the wide range of products available in the market, you need to care about few important things that are given below: Best Family Floater Health Insurance Plans An individual Mediclaim policy provides coverage to you and your family health that offers financial protection against several the medical emergencies. So, if you don’t want to lose your saving or avoid a hole in your pocket due to any medical care requirement by you or your family, you should buy the best family floater health insurance plan in the market. When you and your family are covered under a family floater health plan there is no need to buy Mediclaim Insurance policies for every member of your family. The matter of the fact of buy a single mediclaim policy over a family floater plan is that it is much more nominal than buying individual plan for different members. The premium of Mediclaim Health insurance plan depends up on the number of family member that are covered under the policy, the age of the family members like it considers the age of most senior member. It offers you the sum insured limit for the whole family up to Rs.10 lacs. Benefits of Opting Family Floater Health Insurance Plan Cashless Treatment Allowance This is one of the most important coverage you should look for while buying a family floater health insurance plan for your family. This feature under a health insurance plan allows you to avail cashless treatment at network hospitals of the insurance company. Nominal Premium All the important coverage and benefits that are required by you should be available under a family floater plan that you are buying. But make sure you check the premium amount before you buy the plan. Pre Existing Diseases Family floater health insurance plan also provides coverage for pre-existing diseases after certain waiting period. Claim Settlement Procedure Claim settlement procedure of the insurance company should be very simple and easy. For your convenience I am listing the name of top family floater plan available in the market. But before selecting any plan from the list make sure that you compare these plans on the basis of coverage, benefits and premium. List of Top 5 Family Floater Plan in India 2017

Living with Diabetes is an uphill climb, especially in India where health care is not government-sponsored. Getting a sound health insurance plan is important. But this is not an easy task. Why? Because Diabetes is, unfortunately, not a disease which runs its course eventually. It is an illness that takes permanent residence in your body. It is a disease which takes permanent residence in your body. What’s more, once it settles in, it begins to do its real job. And that is to wreak havoc on all other vital systems.

Long-term complications include kidney failure, stroke, heart disease and eye damage. This is another reason why even the most accommodating insurance companies shy away from providing a comprehensive diabetes insurance plan. Don’t be disheartened. Even though Diabetes is labelled a “high risk” condition, the good news is that it can be controlled. The better news is that there are a few plans which cover it. Now breathe easy and read on. Which types of Diabetes are now covered by health insurance plans? Here, we have the best news for you. Insurance plans nowadays, e.g. Apollo Munich Health Insurance, cover the most common type – Type 2 Diabetes. In addition, this plan also covers Impaired Fasting Glucose (IFG), Impaired Glucose Tolerance (IGT) and/or Hypertension. Appropriately titled their Energy Health Insurance Plan, it offers coverage from Day 1 itself for all hospitalisation due to this condition. What more can a patient ask for? What is wonderful about it is that it’s not only a passive insurance plan. It is more of a wellness plan to monitor your health continuously. Any Diabetes patient will attest to how important this is in their fight to control this disease. They further sweeten the deal by offering 25% discounted premiums if you can show that you manage and control your diabetes well. This is a wonderful double-edged benefit. Not only will your premiums cost less, but you have also taken giant leaps towards better health. Who all are eligible for this plan? This plan covers a very wide demographic, as this disease can strike at any time in one’s adult life. Since its effects are far-reaching and all-encompassing, it is even more important to be financially secure. Eligible ages are as low as 18 years and as high as 65 years. Let’s check out some benefits of this life-saving plan The sum insured ranges from 2 lakhs to 10 lakhs. This often proves enough to cover a host of life-saving procedures and medication. Even though we mentioned this one, it’s so important that we will say it again! The plan offers coverage of all hospitalisation due to Diabetes and Hypertension FROM DAY ONE. We highlighted this for good measure. If we had neon lights, we would have inserted them here. There are two variants to the plan – Gold (wellness test costs included) and Silver (without wellness tests). While the Silver plan is comprehensive in its own right, the Gold plan leaps above and beyond what a good insurance plan ought to be. And why not? Managing Diabetes is not short term. It is a permanent way of life. It has to be monitored and controlled for years on end. If one’s health plan assists in this, what’s not to love about it? The Gold plan thus offers an entire ecosystem of help in controlling this uninvited disease. A personal health coach will guide you throughout the term of your plan. He/she will prescribe the right diet, lifestyle and fitness plans tailor made to suit you. You will have access to a dedicated central helpline to guide you and resolve any concern. Now, help is just a phone call away. Control over your Diabetes is impossible without a steady stream of health supplements, monitoring machines and foods. Your plan offers you a health marketplace with hard-to-resist discounts on all items. You will be provided access to a wellness portal which stores all your medical records and history for quick access. Apollo Munich understands that your valuable time and energy should be spent taking care of yourself. They have removed all hassle from contacting them and offer many channels to touch base easily. They offer a live chat on their website during regular operational hours. In case you missed this, drop them a message, and they will call you back. Apollo Munich Health Insurance renewal is a dream. It’s an easy process with minimal steps on their website. Let’s sum up a few of the salient features from the Apollo health insurance reviews: Types of Diabetes covered Type 2, Impaired Fasting Glucose, Impaired Glucose Tolerance, Hypertension Eligible age 18-65 years Cashless claims Yes Tax benefits Yes, under section 80D Waiting period for claims None for Diabetes complications Renewal period 1 year When your car is valued by an automobile company, your car insurance provider pays you for the evaluated car's value. You can direct this amount toward the money you still owe on the valued car, or you can invest it for purchasing of a new vehicle.

Everyone who has been through this procedure agrees that it is the most frustrating to accept the value of your car evaluated by your car insurance company. The evaluated value of your car comes much lower than what you estimated, which is not at all sufficient to purchase a new car. In many cases it is less than what they still owe on the car. Considering the fact most car owners are clueless of the methodology and terminology used by insurance companies to value cars. The valuation methodology of the car is esoteric, rely on abstract data, the specifics measures of which they are very keen not to reveal. This measures and methods make it difficult for a car owner to raise question on the low offerings from a car insurance company. However, knowing the criteria and terminology up on which the insurance company evaluate the value of cars will help you to understand and estimate the real value more accurately which to negotiable. Read the Valuation Process of your Car When you inform insurance company about your car accident, the company fixes your appointment with an adjuster who assesses the damage of your car. The very first step involved in this procedure is determining whether your car needs valuation. Your insurance company may find it necessary that the car need to be valued even if the damages can be fixed. Generally, the insurance company evaluate a car, in case the expense to repair exceeds 60 to 70%, of its total value. Once the car is totaled, the adjuster then move forward with an appraisal and mention a value to the vehicle. The damage occurred due to an accident is exclusive from the appraisal. Now, the adjuster estimates what nominal cash offer for the car would have been immediately before the accident occurred. Next, the insurance company allows a third-party to claim for its own estimated repair expenses incurred on the car due to the accident. This is measure is take to minimize any appearance of underhandedness or impropriety and to allow the car to go through a different valuation methodology. Actual Cash Value Vs. Replacement Cost I am sure now you wish to know that why there is a difference between actual cash and replacement cost. Here is an answer to this question. There is a huge difference between the value of your car as valued by the insurance company and the actual amount that will incur to purchase a new car. The insurance company offers benefits on the basis of actual cash value (ACV). This amount is determined by the insurance company for someone who reasonably bear for the car, assuming the time before accident. Therefore, the value is considered as depreciation, wear and tear, cosmetic blemishes, mechanical problems and supply and demand in your locality. Even in case you buy a new car and only drove it for a year before the accident took place, its ACV will be less than what you paid for the car. Hope this article has helped you to clear the methodology used to value the car. Now consider the above factors to estimate the value of you car from your end. For further assistance you can also take help from insurance agent or broker. They will help you to understand the terminology and methodology in a better way. The market is becoming expensive day by day and there is no denying the fact that medical costs are always rising. More often than before, people now often have to visit a doctor once in a while as diseases are rising due to undisciplined lifestyle. Therefore, it is imperative to have a health insurance to protect your life. Just like car insurance, a health insurance should be made mandatory by the government.

Let’s have a look at the reasons why a health insurance should be made indispensable. It is because of the many benefits of a health insurance. Benefits of health insurance

Now the question is can every household in India avail the facility of a health insurance? For a long time, there has been the constant need to solve such a paramount issue, so much so, that the Indian government has been pleading the insurance industry to offer a proper health insurance solution. What are the different types of health insurance companies in India?

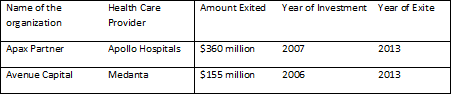

The different types of HDFC health insurance plans are HDFC Ergo Health Suraksha Gold Regain Policy, HDFC Ergo Health Suraksha Regain Policy, HDFC Ergo Health Suraksha Policy, HDFC Ergo Critical Illness Platinum policy, HDFC Ergo Critical Illness Policy, HDFC Ergo Health Suraksha Gold Policy, HDFC Ergo Health Suraksha Top Up Policy, etc. With the passage of time, healthcare expenditures have risen highly. This is why HDFC health insurance plans are aimed towards meeting the healthcare needs of the commoners. Be it HDFC or Bajaj Allianz, IFFCo Tokio, Future Generali, etc., every company has its own schemes included in their health insurance plans. Be aware of the details of the plans and only then purchase it.  Health care is clearly emerging as a big market for private investors, the reason being, very recently some huge name associated with health care sector. No doubt they have earned more than expected value, let’s take few examples below:

The value of exists on this sector goes up from 3 in 2012 to 9 in 2013. Almost ecvery exist have been through secondary sales to different PE funds. All private equity funds investors have found that health care is the primary target to make their investment portfolio. The health care sector has witnesses 16 PE investments between January and March in 2016. Along with some big deals the bullish trends has survived in between April to June in 2016. Related-:Why Innovation in the Health Care Industry Is Difficult Olympus Capital and India Value Fund invested Rs 400 crore in Aster DM Healthcare and Clutch of PE investors in looking to buy stakes in Vasan Healthcare which provides eye care and dental care. According to the study conducted by Global Management consulting firm Bain & Company, consumer and retail goods were the most preferred sector by PE funds in India in 2012. This is how health care became the most favoured sector in Indian market in 2013. Undoubtedly, in the last few years there have been some huge investments made by PE funds in the market, some multinational investors are KKR and Carlyle. According to Neeraj Bharadwaj, Managing Director, Carlyle Asia Partners, on a per capita basis, India have low hospital bed density and low health-care expenses. But increasing per capita income, rising awareness of lifestyle diseases and increasing insurance demands have led to a strong demand for health-care facility in India. “In India the best medical care is offered by private hospitals which insure to offer superior quality health care services and planning to increase its share in the market.” says Mr. Bharadwaj. Multinational investors are not the only ones who are curiously chasing the Indian health-care assets but local investors are also actively participation in healthcare market. The Income Tax Act considers health insurance as a major investment for any individual and hence tax deductions are available under Section 80 D of the act. While insuring yourself, you can save up to Rs 30,000 as tax deductions. But if you think about it should insurance be purchased only to save tax?

Medical expenses are increasing every day and having to pay a huge amount suddenly can be a huge burden on anybody. Individuals insured by health insurance are at ease when such a situation arises as the insurer will support and provide protection. Don’t buy insurance only to save tax but receive benefits of good cover from your policy. Star Health insurance policy offers protection for you, your spouse, dependent children under a single floater policy. The Family Health Optima Insurance plan provides auto-recharge and auto-cover for every newborn in the family. The Star Health insurance renewal process is easy, and a hassle-free process and the Optima policy offer lifetime renewability. Star Health Insurance Review: Key Features Specifications Sum Insured 3 lakhs to 15 lakhs Co-payment 20% of all claims Benefits Hospitalization and Domiciliary treatments Hospital network 6000+ Why to buy the Star Family Health Optima Insurance Plan? Providing up to 405 day care treatments under the policy and automatic restoration of the entire sum insured, the plan provides tax benefits on premium paid. The newborn baby will be covered from the 16th day onwards under the same floater plan, and donor expenses for organ transplantation are covered. Pre-existing diseases are covered after 4 years with any Indian Insurance company pre-hospitalization expenses up to 60 days from the date of hospitalization are covered. Features and Benefits ● Emergency Ambulance Cover up to Rs 750 ● Post-hospitalization expenses up to 90 days from the date of hospitalization ● Recharge Benefit. ● Domiciliary hospitalization expenses exceeding three days. ● In-patient treatment cover included. ● Health check-up expenses cover up to Rs 5000. ● Rooms Boarding, nursing expenses, blood, oxygen, surgeon charges, the cost of medicines and drugs are covered as well. Eligibility Minimum entry age is 5 months while maximum entry age is 65 years. All individuals above 50 years of age who are to be included under the floater policy need to undergo pre-acceptance medical screening, and the cost of while will be borne by the insurer. Newborn babies will be accepted under the policy from the 16th days after birth, and the intimation of the same has to be given to the insurance company. Inclusions The policy covers maximum 5 members, 2 adults and 3 children under a single floater policy. In case the sum insured amount is exhausted by one member of the family, the sum is 100% restored by the insurer. The recharge benefit can be used when the entire sum is not exhausted, and the claim is raised for the same illness by the insured. Without losing your accumulated benefits, you can transfer the policy and also apply to increase the sum during renewal. The Family Health Optima Plan also offers a free look up period of 15 days within which you can demand a refund and stop the policy. Specific diseases such as cataract, hernia, etc. have a waiting period of 2 years. Exclusions ● Mental illness and intentional injury ● Pregnancy, in vitro fertilization, etc. ● Expenses due to war or nuclear accidents. ● Any diseases contracted within 30 days of policy commencement unless accident. ● Change of sex surgery or cosmetic and aesthetic surgery. ● Experimental therapies, naturopathy treatments. Claim Process On hospitalization, contact must be established with the insured to inform about the medical procedure, policy number and other such details. Star health insurance hospital list is available online where cashless facilities can be availed. The documents to be submitted along with the filled claim form are original bills, discharge receipts, investigation reports, doctor’s note and FIR in the case of an accident. The ID card needs to be shown at the desk to avail cashless facilities at network hospitals. Payments by any mode other than cash are eligible for deductions under 80 D and can help you save, but don’t forget insurance is not for tax saving but to protect you in the event of an unforeseen circumstance. While health insurance is an investment, Star Family Health Optima Insurance Plan gives you deductions and protects your family for the future. |

RSS Feed

RSS Feed