|

Nothing is certain in this world. With today’s fast paced life, health often takes a back seat. Sedentary lifestyle, unhealthy food habits, adulteration in edible products, and the general uncertainty of today’s world make a healthy lifestyle a tough ask. Thus, health insurance is a must in today’s day and age. You never know when you might need one. It doesn’t matter what your age is, or whether you are a young I.T professional fresh out of college or a successful businessman making hay while the sun shines, health insurance is a must for all. Online health insurance helps protect one from unexpected medical costs caused due to injuries or other health hazards.

Apollo Munich Medical Insurance Apollo Munich Health Insurance is a joint venture between Munich Health and Apollo Hospitals Group. It is not a standalone health insurance company. Munich Health is a reputed name in the sphere of healthcare all over the world. Apollo Munich offers health insurance and other related products. Apollo Munich offers many different health plans, as specified below. Easy Health Standard Insurance Overview Minimum Entry Age 5 years Maximum Entry 65 years Policy Term 1 or 2 years Minimum Sum Assured Up to 5 lacs Dependent Child Coverage 91st day (when either parent is covered) Why should you buy Easy Health Standard Insurance? The policy offers a reliable health cover. Features

Minimum Entry Age 5 years Maximum Entry 65 years Policy Term 1 or 2 years Minimum Sum Assured Up to 50 lacs Dependent Child Coverage 91st day (when either parent is covered) Why should you buy Easy Health Exclusive Insurance? The policy offers a reliable and extensive health cover. Features

Benefits

Minimum Entry Age 5 years Maximum Entry 65 years Policy Term 1 or 2 years Minimum Sum Assured Up to 50 lacs Dependent Child Coverage 91st day (when coverage is available for either parent) Why should you buy Easy Health Premium Insurance? The policy offers a reliable and widely extensive health cover. Features

No documents needed for policy purchase. Certificate defining your medical fitness is needed after a certain age, as per company policy. Claim Filing Cashless Claim

Reimbursement: Send the claims form, doctor’s certificate and bills to Apollo Munich’s mailing address Claim handling

The health insurance review by Apollo would help you easily decide which health plan to go for.

0 Comments

The medical insurance industry has evolved a lot in the last 5 years. In fact, it has seen an incredible amount of growth since its inception in 1986. Even then, till date, only about 25% of the Indian population is covered under a suitable healthcare plan.

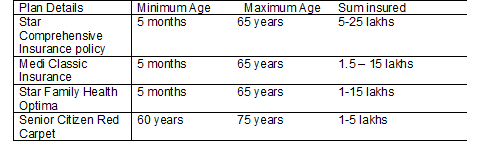

To cover the incidental costs of unexpected medical expenditures, having a health plan for yourself and your family is a must! That is why we bring you a checklist of all things you need to consider when you go out to shop for a personal health cover. 1. The Necessary Cover When deciding on your cover amount, think about the future cost of healthcare. You might be spending not more than a lakh at present on your medical needs, but the amount will only grow as your age progresses! Therefore, instead of buying top-offs in the latter years, it is better to choose a high cover amount now! For a young working professional, managing the premiums for the same would not be an issue. For example, Star Health Insurance offers you a comprehensive choice of insurance covers depending on individual means and needs: Health Plans Minimum (INR) Maximum (INR) Family Health Optima 200,000 1,500,000 Senior Citizens Red Carpet 200,000 1,000,000 Star Comprehensive 500,000 2,500,000 Medi-Classic (Individual) 150,000 1,500,000 Star Health Gain 100,000 500,000 2. Don’t Compare Premiums Don’t compare different health policies based on the premium that needs to be paid. In fact, judge them by what benefits it offers you and your family! For Example, the Family Health Optima plan by Star Health Insurance is an affordable health policy that provides a widespread coverage for that includes your whole family. Some of its highlighting features are:

3. Limitation On Hospitalization Expenses Sometimes, health policies offer a set amount as daily expenses on hospitalization! They do not consider if the procedure is big or small. The difference in the cost would then have to be borne by you! For example, the Family Health Optima policy protects the policyholder against expenses incurred because of a minimum 24-hour in-patient admission. These expenses include the cost of room rent, boarding, and nursing. A cost of doctors, specialists, anaesthetist, surgeons, OT, oxygen, blood, pacemaker, medicines, etc. The cost of room rent covered is equivalent to 2% of the insured sum capped at INR 4,000 each day. Ambulance charge per hospitalization is INR 750, and for every single policy period, it is INR 1,500. Cost accumulated 60 days before getting admitted to the hospital and 90 days after getting discharged are covered under this policy. 4. Cap On Entry Age Illnesses are no longer only age related. Diseases borne because of our lifestyle are cropping up as well. Therefore, choose a health insurance that offers a longer entry age limit. For example, Star Health Insurance maximum entry age for its various policies are: Health Plans Maximum Entry Age (in years) Family Health Optima 65 Senior Citizens Red Carpet 70 Star Comprehensive 65; for dependent children: 25 years Medi-Classic (Individual) 65 Star Health Gain 65 5. Limitations On Treatment If you have a pre-existing condition, check whether that is included in the health plan you are considering. For example, pre-existing illnesses are covered only after 4 years of continuous existence of the Star Health Insurance plan. 6. Health Policy For Parents Ensure that the plan you are considering includes a cover for your parents. For example, insurance plan from Star Health offers a cover for your parents where:

7. Company’s Reputation Check for the claim ratio, online reviews from star health, and customer experiences, of the organization you are thinking of buying your health insurance from. 8. Premium Amount After Age 45 Most health insurers raise the premiums after the policyholder reaches the age of 45. Check to make sure that is not the case with your chosen policy. 9. Extent Of The Health Policy Instead of buying a plan that covers everything, select the one that insures you against major medical expenses. It is up to you to decide whether you want all simple procedures included in your umbrella or not! 10. Exclusions And Waiting Period All insurance policies, health and otherwise, have certain conditions and situations that are excluded from their cover. For some, there is a waiting period before it can be included in the policy cover. You need to be aware of them both so as to know where you stand regarding a particular illness or claim! When you buy an insurance policy, you should be aware of what you are buying and also the terms and conditions related to the plan. There are various reasons why your insurance claim may get rejected. Once you know them you can avoid them.

Reasons why your claim may get rejected

Now, the question is what you can do if your claim gets rejected. There are ways to avert such a sticky situation by the following procedures. Steps taken to ensure that your insurance policy does not get rejected

Thus, follow the above steps to ensure that your insurance claim does not get rejected and you get the claims definitely. Buying a health insurance policy for yourself and your family goes a long way. Not only does it bails you out of a financial crisis during a difficult time, but also contributes to your peace of mind.

What’s more? Any health insurance plan purchased for you and your family will help you in saving money when you pay income tax. Are You a Tax Paying Citizen? Paying income tax is an important duty that everyone must abide by. However, when it comes to parting with hard-earned money, nobody could be blamed for wanting respite. The budget for the year 2015-16 brought numerous alterations, but when it came to income tax, some expectations were not met. The exemption limit was held at INR 2.5 lacs. However, section 80D underwent a major change. You may read an article about health insurance tax benefit 2015 here. Additional Saving of Money Maximum tax deduction under section 80D for FY 2015-16 was increased from INR 15,000 to 25,000. So, considering you fall in the 30% income tax bracket, you are eligible to save a further Rs.3000 if you have a health insurance plan. The increased limit will be applicable for deduction under section 80D for FY 2016-17. The Section for Tax Deductions On Medical Insurance Premium The need to encourage the buying of medical insurance was recognised by the government after the initial years of independence. After that, the section 80D of the Income Tax Act of 1961

For individuals or families where no one is above 60 years of age, the deduction is maximum INR 25,000. For senior citizens, the exemption is more than INR 30,000. The point to note here is that the tax exemption provided is dependent on how much health insurance plan premium you pay. So, if you pay a medical premium of INR 18,000 for self and family, your deduction will be INR 18,000 and not 25,000. Parents’ health insurance premium tax benefit can also be claimed. Consequently, your taxable income can be reduced by further 25 or 30 thousand rupees. This link gives considerable information regarding 80D deduction for AY 2015-16. Features of The Section 80D There is no restriction on which company you buy your health insurance from. Therefore, even the private general insurance companies list the 80D income tax exemption in their benefits. Another aspect to note is that it does not matter what kind of health insurance plan you have. Critical illness policy, accident care plan and all the rest are included. There is a provision for adding a maximum amount of INR 5000 to the tax deduction claim for health check-ups. Although, this is not apart from the maximum 25 or 30 thousand deductions. If you pay a premium of INR 21,000, you can add another INR 4,000 to it if you have undergone a health check-up. Be Aware of These Details You are eligible for the tax benefit if you have taken care not to pay the health insurance plan premium with cash. The section 80DD tax benefit can be availed for specific cases only. Refer here for more information about this section. Employed children cannot be quoted in the deduction claim. Also, the allowed amount under medical check-up is the gross total for the whole family and not per person. Secure The Health of the Family These days, due to the rising medical costs, having a health insurance plan is vital. So taking the multiple covers of a mediclaim policy and the tax benefits into account, getting insured is enormously advantageous. You have to be careful while shopping for the right health insurance plans. There are basically two types of health insurance plans- high deductible and low deductible insurance plans. Your choice is largely determined by your medical situation. Before selecting the right one, you have to know how deductible actually works out.

So, how does deductible work out? Wondering what is a deductible? It is the limit that one has to meet for the insurer to give out benefits. Once after paying the deductible, you may owe some portion of your insurance bill which is known as co-insurance. Under high-deductible plans, co-insurance and co-payments will cost more. An example- Suppose you meet with an accident while running and you fall down and break your leg. Immediately, you are taken to a hospital which comes under the insurance list that you have. In your initial visit, suppose you pay $100. However, after a few months, you are billed with a whopping $2500 that was covered by your plan under 80 percent. So, the question is how does a single short trip result into $2500 bill? Let’s understand this that your deductible is $2000 which is quite high. Now, suppose the hospital charged you a total $4500 for treating your leg. After the deductible, $2500 is the balance that was covered by your plan’s 80 percent. Therefore, co-insurance will allow to reimburse the remaining 20 percent. Therefore, it means you paid $2500, while your insurance carried paid $2000. When to choose low-deductible option and high-deductible option? If you are looking for less financial commitment, the low-deductible option is the best. These types of health plans tend to charge more up front. If you have chronic illness or ongoing medical problems, then the low deductible options are the best. People who often have to visit the doctor for reasons like diabetes, then the low-deductible option is the right one. In this case, premiums are higher but the insurer tends to pay higher percentage for your medical condition. Therefore, opting the low-deductible pay will help you pay less than $1000 for your broken leg. Therefore, to put it in few words, low-deductible is the right option for those having limited savings option. On the other hand, a high deductible plan is suitable for those who seldom have to visit the doctor for poor health. The best part is that you will have to pay lower premiums with these types of high-deductible plans. Since high-deductible plans are aimed for “consumer-directed health plans”, you can think about the right types of healthcare that you want. This type of deductible plan allows you to participate in health savings account. This option allows you to keep pre-tax money aside to meet out-of-pocket expenses. The best part is these accounts earn interests without having to paying tax. In addition to this, your employer may contribute to your consumer-directed health plans. Thus, assessing all your options and the pros and cons of both, you will have to decide which deductible option is for you.  The Oriental Health Insurance reviews to be one of the most well reputed insurance companies based out of India. This organization provides special health insurance products to people of and above the age of 60 years. It provides cashless facilities at most hospitals; however, there are standard guidelines that need to be followed.

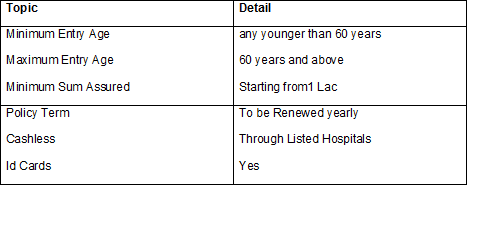

Overview Founded in 1947, the Oriental Health Insurance Co. Ltd has constantly attracted customers hailing from a large demographic audience, enabling the current premium to stand at over Rest 7.282 crores. The Oriental Health Insurance Co Ltd, with its head office in New Delhi, functions independently with a board consisting of prominent personalities like T.A Pai and KR Puri, both accomplishment and respected in their individual fields of interest. Operational internationally, the Oriental Health Insurance reviews to be reputed in its work in the health insurance sector. Why to Buy Oriental Health Insurance? The Oriental Health Insurance provides cashless services at selected specialty hospitals. It insures customers who are 60 years and older. It is a well-reputed company with experts I the field that will be able to advise the customer effectively. Features, Benefits, and Inclusions of Oriental Health Insurance The Oriental Health Insurance aims to bear the following features, benefits, and inclusions.

People wanting to buy this policy will have to undergo a few medical tests, like a series of blood test and USGs. This is particularly for those above the age of 45. Documents Required The following are required for age proof:

Following are some of the points that will not be included as part of the policy:

To claim the Insurance in the case of hospitalization, the original bills, doctor’s certificate, discharge certificate, test reports and relevant documents from the doctors are needed. All documents must be self-attested and submitted to the company within 7-60 days of the incident. All documents that will assist in the company passing the claim.  With increasing awareness regarding purchasing health insurances, reliability on group covers provided by employers is decreasing. Group covers have a lot of exclusions and the policies provided by the employer might not cover the required benefits.

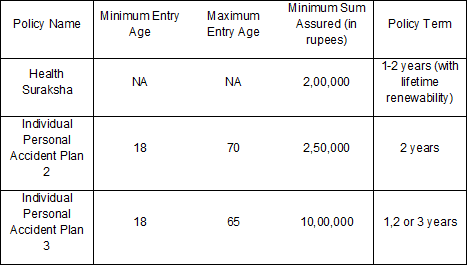

Overview of HDFC Insurance Reviews Why buy Individual Personal Accident Plan 3? Accidents are disastrous, unforeseen events that affect the monetary security of a family. In order to provide the best protection to one’s family, Individual Personal Accident Plan 3 has received the best HDFC insurance reviews. Not only does it provide financial stability in case of death, but also for permanent disabilities, burns, and physical injuries. Features and Benefits Let's have a look at the HDFC Insurance Reviews. The cover provided is applicable 24 hours a day, seven days a week, 365 days a year. The individual is insured by this Personal Accident cover in India as well as any other location worldwide. No prior health check-up is required. Lifetime renewability applies to this policy. Eligibility

Coverages from 10 to 25 Lacs Sum insured

All the above-mentioned benefits are covered in this advanced scheme. In addition to that, HDFC insurance reviews have shown that the following benefits are also covered:

Bodily Injury / Sickness caused:

A claim can be easily placed by calling HDFC Toll free numbers:

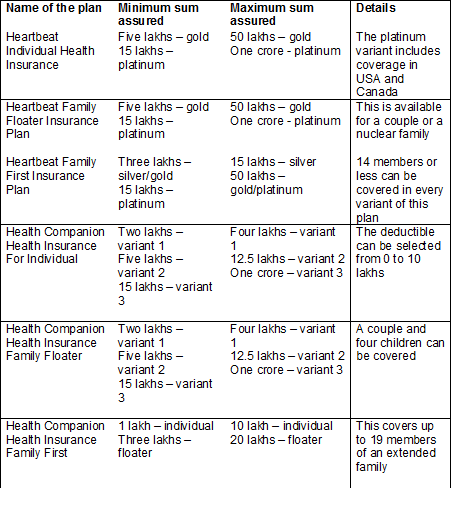

Max Bupa is an established company in India. All of its health insurance products are beneficial to the customers. The products come in 3 different sections, plans for individuals, plans for family and extended family and fixed benefit plans.

Here Is an Overview Of The Max Bupa Insurance Plans The Heartbeat plan can be bought for an individual, a couple, a nuclear family or an extended family. However, the variants and sum assured for any plan are different and customizable. You can read a Max Bupa Health Insurance review for heartbeat policy here. The Max Bupa Health Companion Health Insurance plan comes with the deductible option. Why to Buy The Max Bupa Health Assurance Insurance Plan? Max Bupa Limited provides the best health insurance policies in India. The fixed benefit plans are named Health Assurance Insurance Plans. These plans each cover three different coverage options. 18 to 65 years is the eligible age range for the customers. The first one is CritiCare, with which you can get financial help if you have been diagnosed with a critical illness. But the illness has to be among the 20 listed in the terms of the policy. With AccidentCare, you can get monetary respite if you have been permanently disabled in some way. The HospiCash option can be selected if you want a daily cash benefit. Children between 5 and 21 years can also avail AccidentCare and HospiCash Health Assurance policy. The Unique Features and Benefits

Eligibility The eligibility in terms of age is mentioned above. But some eligibility terms stand for the benefits as well. You can read all the terms and conditions on the website before buying. Inclusions The coverage and inclusions for each plan are different. For instance, the heartbeat plans include maternity benefits, and the companion plans include pre and post hospitalization expenses. The Max Bupa Health Insurance plans are income tax deductible. Read Exclusions Carefully There are some cases in which your insurance claim will be disapproved. These exclusions are common to each plan and clearly mentioned while buying the policies. Some of those are drug abuse, cosmetic surgery, sexually transmitted diseases and psychiatric conditions. You can view the whole list in the Max Bupa Health Insurance brochure. Documents Required If you are hospitalized in one of the 3500 hospitals that Max Bupa has a tie up with, you will not require many documents. But for reimbursement claim in any other hospital, Max Bupa Health Insurance claim form is a major document required during the process. Claim Process The procedure is not very difficult. This link will give you all the information that you will need. Or you could look at any Max Bupa Health Insurance review to know more.  Life is indeed uncertain, but your decisions don’t have to be. Are you searching for best health plans, clicking every Google results and yet jumbled which one to choose from? With so many best health insurance plans in India, confusion is considerable. Here are some health insurance reviews indicating why you should consider Star Health Insurance Plans for your future self and family. Let’s take a bird’s eye view of its various plans and relevant details What makes Star Health most preferred? Among all the health insurance reviews we found Star Health Insurance review to be most versatile. It is India’s first stand-alone insurance company. They are top rated health insurance provider and hence offer health insurance, personal accident, and overseas mediclaim through its around 6,000 strong hospital networks. It is considered to bear the best family floater health insurance plan in India. In April 2013, they launched special policy for people suffering from cardiac ailment becoming first among the others.They also propose one of the best individual health insurance among other top health insurance companies in the nation. Key features which attract most of the insurances There are many categorizations such as Comprehensive Plans, Medi Classic Plans, Family Delite Insurance, and Senior Citizen Red Carpet, etc. makes it most accepted health insurances nationwide. There are further variants of travel plans such as Star student travel, Star Family travel, etc. to be the renowned ones. It has a term of the policy for one year and includes Renewal coverage for whole life.They also provide provisions of going cashless treatment facility. Eligibility The Age eligibility is from 5 months to 65 years. There are two subgroups including individual and family floater. The family Floater includes a maximum of 4 members in the family including two adults and two children. Inclusions in the insurance policy

Although getting insured by Star Health is an easy process but an individual needs to submit various documents in the beginning or during claims. The same can be verified by the given official link of the company Star Health Insurance claim is as easy to go In the case of a planned hospitalization of the person, the person has to fax the Pre-authorization form duly completed from the hospital. They further have to carry respective ID proofs and policy schedule. In the case of emergency, the person avails the treatment and later fax the Pre-authorization form duly filled from the hospital within twenty-four hours of admission. There is also Reimbursement claim in which the insured avails the treatment, pays the expenses and claims the reimbursement of the expenses later. When one is buying accident insurance cover policy he or she will be covered against the accidental death. The policy also offers coverage against disability that one incurs due to accident. With accident insurance plan one is protected from spending money in medical expenses. Unlike earlier days people are likely to be subjected to accidents at any point of time and the rate of accidents has increased beyond imagination. Here minor accidents are not talked about but the major ones which either snatch away life or drive one lead life as disable.

Accidents affect well being and livelihood. All one needs an all inclusive insurance plan to be protected from all kinds of unwarranted medical expenses. When a sound medical insurance policy is purchased one can stay safe from all kinds of financial repercussions. After all the value of human life is immeasurable and such policies are known to render some peace of mind to those who are dependent, so insurance companies have devised such policies which would be compensating one on the event of sudden demise, physical damage and mutilation. So when an individual fall victim to situations such as violence, natural calamity or road accident. The policy would be guarding those who were dependent upon the victim from coming under any economic repercussion. The injury may take place in air, rail or road anywhere but this policy helps in shielding the family. Varying Insurers with varying schemes There are insuring companies like HDFC Ergo General Insurance, New India Assurance, Royal Sundara, General Insurance, SBI General Insurance, Max Bupa Health Insurance, ICICI Loambard General Insurance and many more. The age group for enjoying this policy is restricted to 18-65 years. Types of insurance policies

What the policy exactly covers When there is accidental death, accidental dismemberment, terrorism act, accidental disability, regular payment during hospitalization. These are the areas where the policy holder may expect to get help from personal accident insurance plans. These plans are practically prepared so that one would be helped in time of need. Advantages of having accident insurance The insurance policy helps in meeting bank EMIs, varying expenditures and medicinal costs. With such policies, one would be enjoying number of advantages:

|

RSS Feed

RSS Feed