|

When your car is valued by an automobile company, your car insurance provider pays you for the evaluated car's value. You can direct this amount toward the money you still owe on the valued car, or you can invest it for purchasing of a new vehicle.

Everyone who has been through this procedure agrees that it is the most frustrating to accept the value of your car evaluated by your car insurance company. The evaluated value of your car comes much lower than what you estimated, which is not at all sufficient to purchase a new car. In many cases it is less than what they still owe on the car. Considering the fact most car owners are clueless of the methodology and terminology used by insurance companies to value cars. The valuation methodology of the car is esoteric, rely on abstract data, the specifics measures of which they are very keen not to reveal. This measures and methods make it difficult for a car owner to raise question on the low offerings from a car insurance company. However, knowing the criteria and terminology up on which the insurance company evaluate the value of cars will help you to understand and estimate the real value more accurately which to negotiable. Read the Valuation Process of your Car When you inform insurance company about your car accident, the company fixes your appointment with an adjuster who assesses the damage of your car. The very first step involved in this procedure is determining whether your car needs valuation. Your insurance company may find it necessary that the car need to be valued even if the damages can be fixed. Generally, the insurance company evaluate a car, in case the expense to repair exceeds 60 to 70%, of its total value. Once the car is totaled, the adjuster then move forward with an appraisal and mention a value to the vehicle. The damage occurred due to an accident is exclusive from the appraisal. Now, the adjuster estimates what nominal cash offer for the car would have been immediately before the accident occurred. Next, the insurance company allows a third-party to claim for its own estimated repair expenses incurred on the car due to the accident. This is measure is take to minimize any appearance of underhandedness or impropriety and to allow the car to go through a different valuation methodology. Actual Cash Value Vs. Replacement Cost I am sure now you wish to know that why there is a difference between actual cash and replacement cost. Here is an answer to this question. There is a huge difference between the value of your car as valued by the insurance company and the actual amount that will incur to purchase a new car. The insurance company offers benefits on the basis of actual cash value (ACV). This amount is determined by the insurance company for someone who reasonably bear for the car, assuming the time before accident. Therefore, the value is considered as depreciation, wear and tear, cosmetic blemishes, mechanical problems and supply and demand in your locality. Even in case you buy a new car and only drove it for a year before the accident took place, its ACV will be less than what you paid for the car. Hope this article has helped you to clear the methodology used to value the car. Now consider the above factors to estimate the value of you car from your end. For further assistance you can also take help from insurance agent or broker. They will help you to understand the terminology and methodology in a better way.

0 Comments

The market is becoming expensive day by day and there is no denying the fact that medical costs are always rising. More often than before, people now often have to visit a doctor once in a while as diseases are rising due to undisciplined lifestyle. Therefore, it is imperative to have a health insurance to protect your life. Just like car insurance, a health insurance should be made mandatory by the government.

Let’s have a look at the reasons why a health insurance should be made indispensable. It is because of the many benefits of a health insurance. Benefits of health insurance

Now the question is can every household in India avail the facility of a health insurance? For a long time, there has been the constant need to solve such a paramount issue, so much so, that the Indian government has been pleading the insurance industry to offer a proper health insurance solution. What are the different types of health insurance companies in India?

The different types of HDFC health insurance plans are HDFC Ergo Health Suraksha Gold Regain Policy, HDFC Ergo Health Suraksha Regain Policy, HDFC Ergo Health Suraksha Policy, HDFC Ergo Critical Illness Platinum policy, HDFC Ergo Critical Illness Policy, HDFC Ergo Health Suraksha Gold Policy, HDFC Ergo Health Suraksha Top Up Policy, etc. With the passage of time, healthcare expenditures have risen highly. This is why HDFC health insurance plans are aimed towards meeting the healthcare needs of the commoners. Be it HDFC or Bajaj Allianz, IFFCo Tokio, Future Generali, etc., every company has its own schemes included in their health insurance plans. Be aware of the details of the plans and only then purchase it.  Health care is clearly emerging as a big market for private investors, the reason being, very recently some huge name associated with health care sector. No doubt they have earned more than expected value, let’s take few examples below:

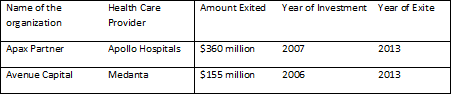

The value of exists on this sector goes up from 3 in 2012 to 9 in 2013. Almost ecvery exist have been through secondary sales to different PE funds. All private equity funds investors have found that health care is the primary target to make their investment portfolio. The health care sector has witnesses 16 PE investments between January and March in 2016. Along with some big deals the bullish trends has survived in between April to June in 2016. Related-:Why Innovation in the Health Care Industry Is Difficult Olympus Capital and India Value Fund invested Rs 400 crore in Aster DM Healthcare and Clutch of PE investors in looking to buy stakes in Vasan Healthcare which provides eye care and dental care. According to the study conducted by Global Management consulting firm Bain & Company, consumer and retail goods were the most preferred sector by PE funds in India in 2012. This is how health care became the most favoured sector in Indian market in 2013. Undoubtedly, in the last few years there have been some huge investments made by PE funds in the market, some multinational investors are KKR and Carlyle. According to Neeraj Bharadwaj, Managing Director, Carlyle Asia Partners, on a per capita basis, India have low hospital bed density and low health-care expenses. But increasing per capita income, rising awareness of lifestyle diseases and increasing insurance demands have led to a strong demand for health-care facility in India. “In India the best medical care is offered by private hospitals which insure to offer superior quality health care services and planning to increase its share in the market.” says Mr. Bharadwaj. Multinational investors are not the only ones who are curiously chasing the Indian health-care assets but local investors are also actively participation in healthcare market. The Income Tax Act considers health insurance as a major investment for any individual and hence tax deductions are available under Section 80 D of the act. While insuring yourself, you can save up to Rs 30,000 as tax deductions. But if you think about it should insurance be purchased only to save tax?

Medical expenses are increasing every day and having to pay a huge amount suddenly can be a huge burden on anybody. Individuals insured by health insurance are at ease when such a situation arises as the insurer will support and provide protection. Don’t buy insurance only to save tax but receive benefits of good cover from your policy. Star Health insurance policy offers protection for you, your spouse, dependent children under a single floater policy. The Family Health Optima Insurance plan provides auto-recharge and auto-cover for every newborn in the family. The Star Health insurance renewal process is easy, and a hassle-free process and the Optima policy offer lifetime renewability. Star Health Insurance Review: Key Features Specifications Sum Insured 3 lakhs to 15 lakhs Co-payment 20% of all claims Benefits Hospitalization and Domiciliary treatments Hospital network 6000+ Why to buy the Star Family Health Optima Insurance Plan? Providing up to 405 day care treatments under the policy and automatic restoration of the entire sum insured, the plan provides tax benefits on premium paid. The newborn baby will be covered from the 16th day onwards under the same floater plan, and donor expenses for organ transplantation are covered. Pre-existing diseases are covered after 4 years with any Indian Insurance company pre-hospitalization expenses up to 60 days from the date of hospitalization are covered. Features and Benefits ● Emergency Ambulance Cover up to Rs 750 ● Post-hospitalization expenses up to 90 days from the date of hospitalization ● Recharge Benefit. ● Domiciliary hospitalization expenses exceeding three days. ● In-patient treatment cover included. ● Health check-up expenses cover up to Rs 5000. ● Rooms Boarding, nursing expenses, blood, oxygen, surgeon charges, the cost of medicines and drugs are covered as well. Eligibility Minimum entry age is 5 months while maximum entry age is 65 years. All individuals above 50 years of age who are to be included under the floater policy need to undergo pre-acceptance medical screening, and the cost of while will be borne by the insurer. Newborn babies will be accepted under the policy from the 16th days after birth, and the intimation of the same has to be given to the insurance company. Inclusions The policy covers maximum 5 members, 2 adults and 3 children under a single floater policy. In case the sum insured amount is exhausted by one member of the family, the sum is 100% restored by the insurer. The recharge benefit can be used when the entire sum is not exhausted, and the claim is raised for the same illness by the insured. Without losing your accumulated benefits, you can transfer the policy and also apply to increase the sum during renewal. The Family Health Optima Plan also offers a free look up period of 15 days within which you can demand a refund and stop the policy. Specific diseases such as cataract, hernia, etc. have a waiting period of 2 years. Exclusions ● Mental illness and intentional injury ● Pregnancy, in vitro fertilization, etc. ● Expenses due to war or nuclear accidents. ● Any diseases contracted within 30 days of policy commencement unless accident. ● Change of sex surgery or cosmetic and aesthetic surgery. ● Experimental therapies, naturopathy treatments. Claim Process On hospitalization, contact must be established with the insured to inform about the medical procedure, policy number and other such details. Star health insurance hospital list is available online where cashless facilities can be availed. The documents to be submitted along with the filled claim form are original bills, discharge receipts, investigation reports, doctor’s note and FIR in the case of an accident. The ID card needs to be shown at the desk to avail cashless facilities at network hospitals. Payments by any mode other than cash are eligible for deductions under 80 D and can help you save, but don’t forget insurance is not for tax saving but to protect you in the event of an unforeseen circumstance. While health insurance is an investment, Star Family Health Optima Insurance Plan gives you deductions and protects your family for the future. Nothing is certain in this world. With today’s fast paced life, health often takes a back seat. Sedentary lifestyle, unhealthy food habits, adulteration in edible products, and the general uncertainty of today’s world make a healthy lifestyle a tough ask. Thus, health insurance is a must in today’s day and age. You never know when you might need one. It doesn’t matter what your age is, or whether you are a young I.T professional fresh out of college or a successful businessman making hay while the sun shines, health insurance is a must for all. Online health insurance helps protect one from unexpected medical costs caused due to injuries or other health hazards.

Apollo Munich Medical Insurance Apollo Munich Health Insurance is a joint venture between Munich Health and Apollo Hospitals Group. It is not a standalone health insurance company. Munich Health is a reputed name in the sphere of healthcare all over the world. Apollo Munich offers health insurance and other related products. Apollo Munich offers many different health plans, as specified below. Easy Health Standard Insurance Overview Minimum Entry Age 5 years Maximum Entry 65 years Policy Term 1 or 2 years Minimum Sum Assured Up to 5 lacs Dependent Child Coverage 91st day (when either parent is covered) Why should you buy Easy Health Standard Insurance? The policy offers a reliable health cover. Features

Minimum Entry Age 5 years Maximum Entry 65 years Policy Term 1 or 2 years Minimum Sum Assured Up to 50 lacs Dependent Child Coverage 91st day (when either parent is covered) Why should you buy Easy Health Exclusive Insurance? The policy offers a reliable and extensive health cover. Features

Benefits

Minimum Entry Age 5 years Maximum Entry 65 years Policy Term 1 or 2 years Minimum Sum Assured Up to 50 lacs Dependent Child Coverage 91st day (when coverage is available for either parent) Why should you buy Easy Health Premium Insurance? The policy offers a reliable and widely extensive health cover. Features

No documents needed for policy purchase. Certificate defining your medical fitness is needed after a certain age, as per company policy. Claim Filing Cashless Claim

Reimbursement: Send the claims form, doctor’s certificate and bills to Apollo Munich’s mailing address Claim handling

The health insurance review by Apollo would help you easily decide which health plan to go for. The medical insurance industry has evolved a lot in the last 5 years. In fact, it has seen an incredible amount of growth since its inception in 1986. Even then, till date, only about 25% of the Indian population is covered under a suitable healthcare plan.

To cover the incidental costs of unexpected medical expenditures, having a health plan for yourself and your family is a must! That is why we bring you a checklist of all things you need to consider when you go out to shop for a personal health cover. 1. The Necessary Cover When deciding on your cover amount, think about the future cost of healthcare. You might be spending not more than a lakh at present on your medical needs, but the amount will only grow as your age progresses! Therefore, instead of buying top-offs in the latter years, it is better to choose a high cover amount now! For a young working professional, managing the premiums for the same would not be an issue. For example, Star Health Insurance offers you a comprehensive choice of insurance covers depending on individual means and needs: Health Plans Minimum (INR) Maximum (INR) Family Health Optima 200,000 1,500,000 Senior Citizens Red Carpet 200,000 1,000,000 Star Comprehensive 500,000 2,500,000 Medi-Classic (Individual) 150,000 1,500,000 Star Health Gain 100,000 500,000 2. Don’t Compare Premiums Don’t compare different health policies based on the premium that needs to be paid. In fact, judge them by what benefits it offers you and your family! For Example, the Family Health Optima plan by Star Health Insurance is an affordable health policy that provides a widespread coverage for that includes your whole family. Some of its highlighting features are:

3. Limitation On Hospitalization Expenses Sometimes, health policies offer a set amount as daily expenses on hospitalization! They do not consider if the procedure is big or small. The difference in the cost would then have to be borne by you! For example, the Family Health Optima policy protects the policyholder against expenses incurred because of a minimum 24-hour in-patient admission. These expenses include the cost of room rent, boarding, and nursing. A cost of doctors, specialists, anaesthetist, surgeons, OT, oxygen, blood, pacemaker, medicines, etc. The cost of room rent covered is equivalent to 2% of the insured sum capped at INR 4,000 each day. Ambulance charge per hospitalization is INR 750, and for every single policy period, it is INR 1,500. Cost accumulated 60 days before getting admitted to the hospital and 90 days after getting discharged are covered under this policy. 4. Cap On Entry Age Illnesses are no longer only age related. Diseases borne because of our lifestyle are cropping up as well. Therefore, choose a health insurance that offers a longer entry age limit. For example, Star Health Insurance maximum entry age for its various policies are: Health Plans Maximum Entry Age (in years) Family Health Optima 65 Senior Citizens Red Carpet 70 Star Comprehensive 65; for dependent children: 25 years Medi-Classic (Individual) 65 Star Health Gain 65 5. Limitations On Treatment If you have a pre-existing condition, check whether that is included in the health plan you are considering. For example, pre-existing illnesses are covered only after 4 years of continuous existence of the Star Health Insurance plan. 6. Health Policy For Parents Ensure that the plan you are considering includes a cover for your parents. For example, insurance plan from Star Health offers a cover for your parents where:

7. Company’s Reputation Check for the claim ratio, online reviews from star health, and customer experiences, of the organization you are thinking of buying your health insurance from. 8. Premium Amount After Age 45 Most health insurers raise the premiums after the policyholder reaches the age of 45. Check to make sure that is not the case with your chosen policy. 9. Extent Of The Health Policy Instead of buying a plan that covers everything, select the one that insures you against major medical expenses. It is up to you to decide whether you want all simple procedures included in your umbrella or not! 10. Exclusions And Waiting Period All insurance policies, health and otherwise, have certain conditions and situations that are excluded from their cover. For some, there is a waiting period before it can be included in the policy cover. You need to be aware of them both so as to know where you stand regarding a particular illness or claim! |

RSS Feed

RSS Feed